-

Galvanized and Prepainted Steel Selection Guide

Galvanized and Prepainted Steel Selection Guide

-

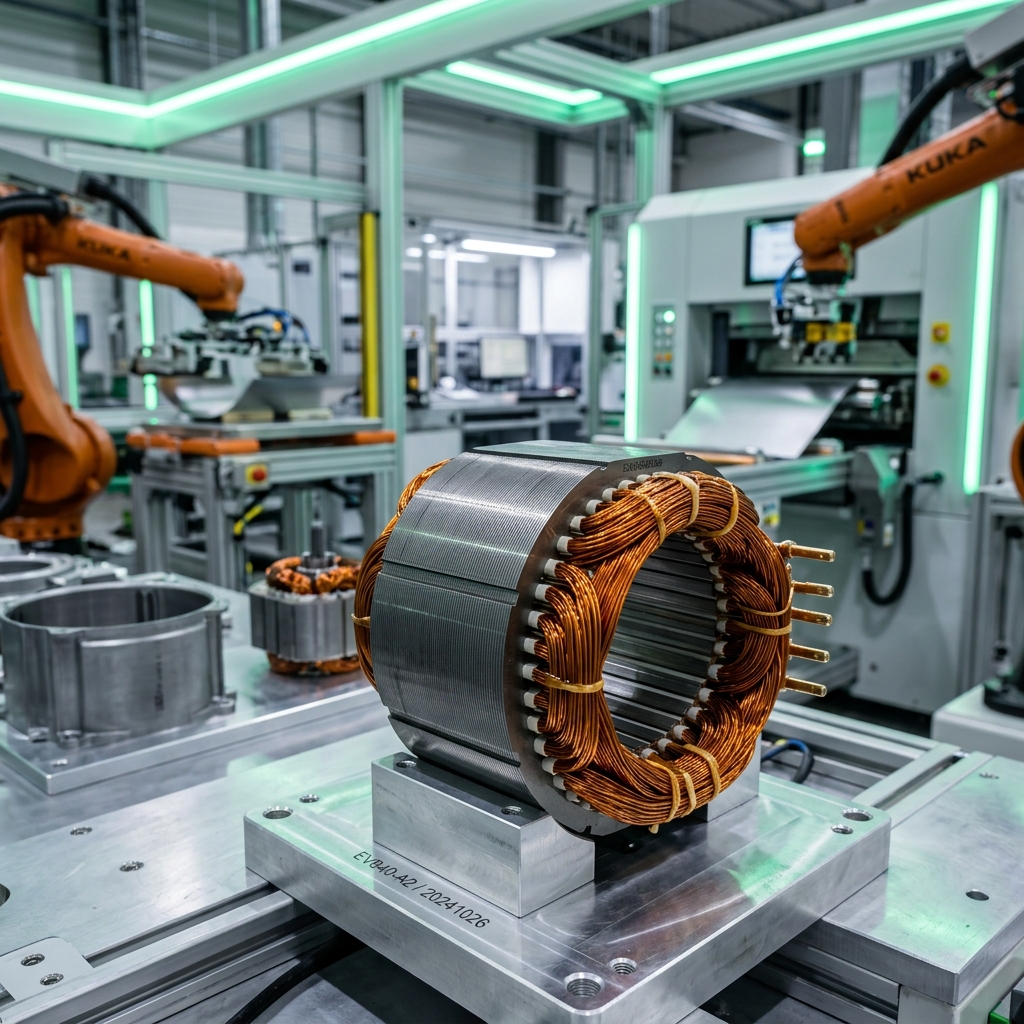

Silicon & Cold Rolled Steel in Energy Efficiency

Silicon & Cold Rolled Steel in Energy Efficiency

-

- Guide

- CHY Engineering Team

The first quarter of 2026 has become a turning point where global geopolitical balances and industrial supply chains were shaken with unprecedented speed. Operation "Epic Fury," which began on February 28, 2026, not only triggered a regional conflict but also led to the de facto closure of the Strait of Hormuz, the jugular vein of global commodity markets. This has brought about a massive logistical and raw material crisis affecting approximately 10% of world steel trade.

Operation Epic Fury and the New Geopolitical Reality in the Middle East

The airstrikes that began on the morning of February 28, 2026, fundamentally changed the status quo in the region. The intervention aimed at Iran's military and nuclear infrastructure created a leadership vacuum, while retaliatory strikes targeted critical energy facilities in the region. These military dynamics are the result of the failure of the 2025-2026 nuclear negotiations, and the borders of the conflict are expanding unpredictably. With the outbreak of the war, global oil prices rapidly surpassed the $100 mark, fundamentally shaking the cost structure for energy-intensive steel production.

The Strait of Hormuz: When the Jugular Vein of Global Trade is Cut

The Strait of Hormuz, through which 20% of the world's oil trade passes, became the biggest bottleneck in global trade as of March 2026. Rather than a physical blockade, insurance cancellations and risk perception have paralyzed traffic. As major maritime insurance organizations suspended war risk coverages in the region, vessel passages almost came to a halt.

The "Perfect Storm" in the Steel Sector: Energy and Production Costs

In March 2026, crude oil settling around $100 and European natural gas prices (TTF) increasing by 80% in just a few days pushed cost curves upwards. Facilities producing with Electric Arc Furnace (EAF) and the DRI method, which is critical for the green steel transformation, have been the segment that took the heaviest blow from this volatility.

- Blast Furnace (BF-BOF): The cost increase remained limited at 2-3%; this increase is mainly due to logistical delays.

- Gas-Based DRI-EAF: Due to the extreme jump in natural gas prices, there is a specific increase of 4-5% in production costs.

The Collapse of the Iranian Steel Industry and the Global Supply Gap

Production in Iran, the world's 10th largest producer, has been paralyzed. The capacity of giants like Mobarakeh Steel has declined to 1% due to energy cuts and infrastructure damage. The halt of Iran's annual export volume of approximately 11 million tons created a "slab panic," especially in the Southeast Asian market. Rolling mills in the region were forced to turn to more expensive alternatives from India and China instead of cheap semi-finished products from Iran.

Turkish Steel Industry: Risks, Opportunities, and Strategic Maneuvers

Turkey is one of the actors feeling the crisis most intensely due to its geographical proximity and energy dependence. According to TCUD and CIB data, Turkish producers have shifted to a strategy of focusing on "near markets" (Europe and the Balkans) where their logistical advantage is maintained. Iran's withdrawal from the European and ASEAN markets could open a new window of opportunity for Turkish steel under EU quotas. However, the use of the Cape of Good Hope route for raw material supply increases costs by $45-65 per ton.

Specialized Steel Producers and the Value-Added Segment Perspective

For high-tech organizations offering special laminated metals, coated stainless steels, and anti-fingerprint solutions, this crisis has brought raw material stability to the forefront. Fluctuations in crude steel production have made supply chain management critical in the value-added product segment.

Conclusion: Future Scenarios and Action Plan for the Steel Industry

The 2026 crisis has shown that survival in the steel sector is possible not only with low costs but with geopolitical agility. The Cape of Good Hope route becoming standard procedure, hedging energy risks, and transitioning to value-added products will determine the sector's new course. It is no longer an option but a necessity for sector representatives to accelerate energy efficiency investments and diversify raw material sources during this period.

CHY Steel Service Center offers high-precision steel solutions to the automotive, white goods, and construction sectors with over 40 years of experience.

CHY Steel Service Center provides high-precision steel solutions to the automotive, white goods, and construction sectors with over 40 years of experience.

View all posts